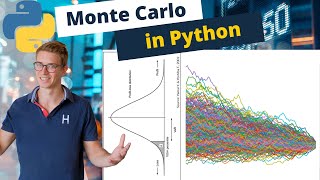

Media Summary: Ever wondered what Value at Risk (VaR) or In today's video we follow on from the Monte Carlo Simulation of a Stock Portfolio in Python and calculate the Hello Candidates, In this video we will be talking about the concept of

Conditional Value At Risk Expected - Detailed Analysis & Overview

Ever wondered what Value at Risk (VaR) or In today's video we follow on from the Monte Carlo Simulation of a Stock Portfolio in Python and calculate the Hello Candidates, In this video we will be talking about the concept of Designed for CFA and FRM Part 1 candidates, this video clearly and simply explains the